SCHOOL PROFILE · FREE PREVIEW

SCHOOL PROFILE · FREE PREVIEW

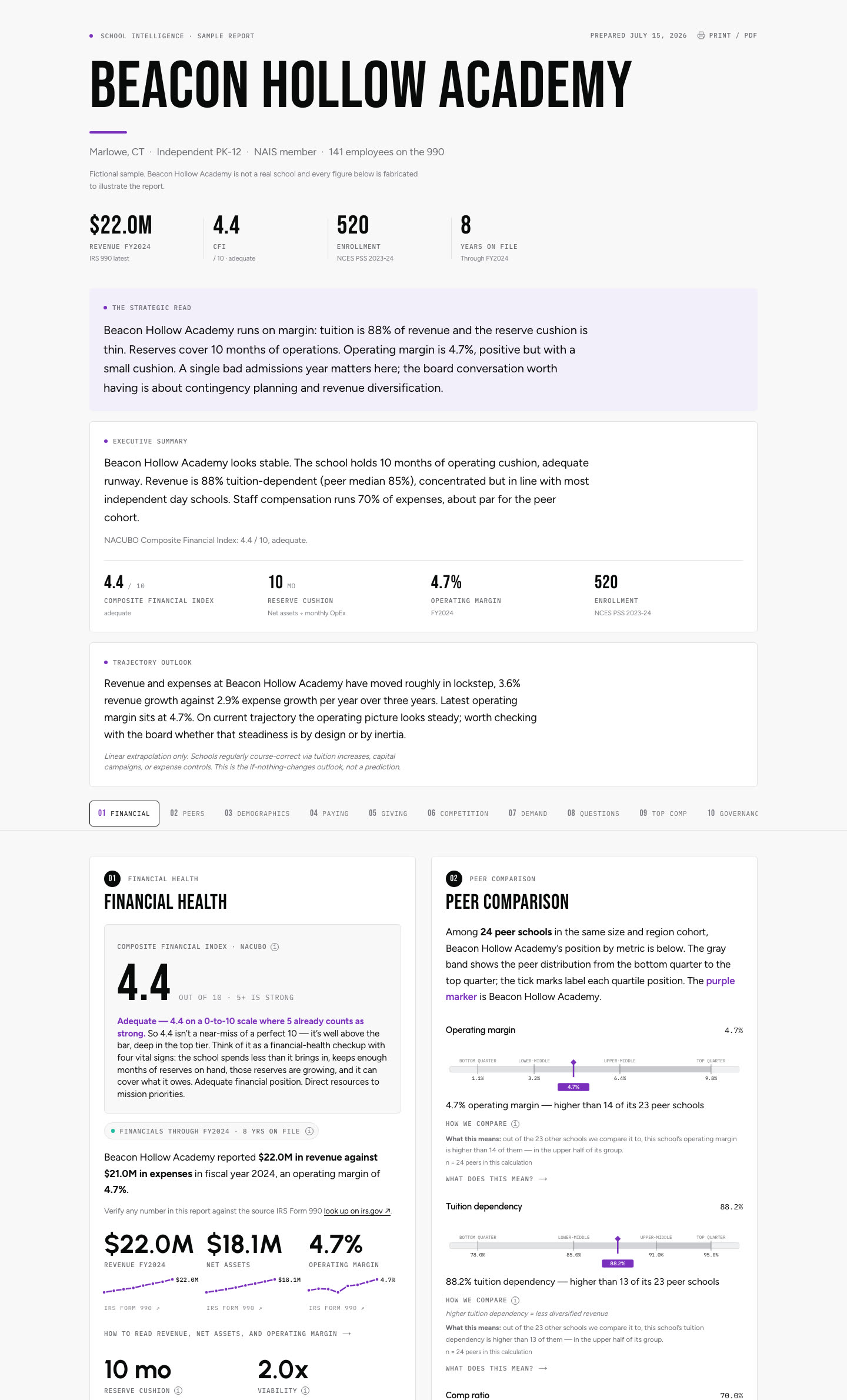

Wichita Christian School-Wichita Falls

Wichita Falls, TX · Independent school

THE READ · FREE SUMMARY

Wichita Christian School-Wichita Falls looks durable. The school holds 2.2 years of operating cushion, a healthy buffer. Revenue is unusually diversified at 58% tuition-dependent (peer median 88%). Staff compensation runs 70% of expenses, generous relative to peers. Net assets are growing 6.1%/yr over three years; the cushion is being built, not drawn. NACUBO Composite Financial Index: 9.4 / 10, strong.

Wichita Christian School-Wichita Falls reported $3.7M in revenue against $2.9M in expenses in fiscal year 2023, the most recent filing on record. Net assets stood at $6.5M — about 2.23x annual operating expense.

Operating margin landed at 21.5%, with 57.9% of revenue coming from tuition. Among same-size peers, that puts Wichita Christian School-Wichita Falls at the p86 on operating margin.

$3.7M

REVENUE FY2023

21.5%

OP MARGIN

20

PEERS RESOLVED

IRS FORM 990 · DATA THROUGH FY2023

THE FULL REPORT

Subscribe to see the full report.

Ten panels on Wichita Christian School-Wichita Falls: financial health, peer comparison, community demographics, paying & giving capacity, competitive position, enrollment demand, leadership compensation, governance — and the questions to ask. One subscription opens every school.

ANNUAL SUBSCRIPTION · CANCEL ANYTIME · 99 FOUNDING SPOTS LEFT

WHERE THIS SCHOOL SITS · REVENUE SCALE VS PEERS

Among 20 similar peer schools, Wichita Christian School-Wichita Falls ranks 13th by latest 990 revenue.

Revenue scale

WHAT’S IN THE REPORT

- Financials — IRS Form 990, up to nine years on file.

- Enrollment & demand — IRS 990 tuition revenue + U.S. Census county births.

- Competition — NCES private (PSS) + public (CCD) school inventory.

- Demographics — U.S. Census Bureau, ACS 5-year estimates.

- Local economy — U.S. Bureau of Labor Statistics, QCEW and CES.

- Peer set — 1,620 independent schools with verified financials.

The full school report

Ten panels. One school. A year of access.

$250 a year — or $100 the first year for the founding 100.

ANNUAL SUBSCRIPTION · $100 FIRST YEAR FOR FOUNDING MEMBERS · CANCEL ANYTIME · 99 FOUNDING SPOTS LEFT